Both Ohio Transfer on Death (TOD) affidavits and revocable living trusts can keep your Columbus, Dublin, or other Ohio home out of probate, but they work very differently. For many Ohio families with at least one home plus investments, retirement accounts, and complex family situations, a living trust usually offers more control and protection than relying only on a TOD.

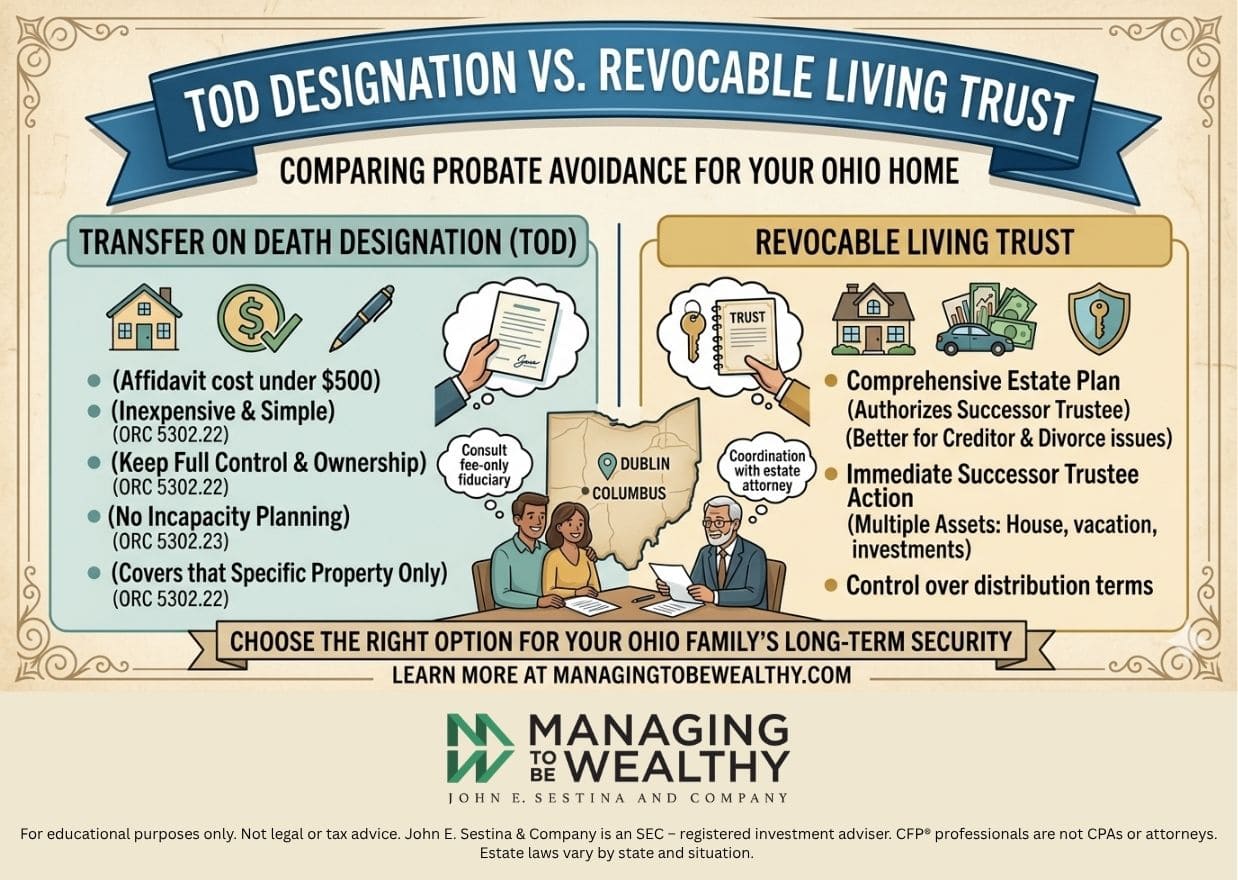

- A transfer on death deed (called a TOD Designation Affidavit in Ohio) is inexpensive and simple for a single home and one adult beneficiary, typically costing under $500 including recording fees. However, the availability of TODDs varies by state and not all states allow them, so it’s important to check Ohio law before proceeding.

- A revocable living trust is better for incapacity planning, multiple beneficiaries, creditor issues, and coordinating multiple assets across your entire estate.

- Ohio law has specific rules for TOD affidavits on real estate under ORC 5302.22, requiring proper recording before death. This requirement applies specifically to Ohio and may differ in other states.

- Neither tool protects assets from Medicaid recovery without more advanced planning. To create a TOD, you must prepare and file the appropriate legal forms with the county office.

- Readers should not change deeds or set up trusts without discussing tax, estate, and financial planning impacts with qualified professionals—an estate planning attorney plus a fee-only fiduciary advisor. When using a trust, you must add new assets to the trust as your estate changes to ensure proper coverage.

Introduction: Why Your Ohio Home Needs a Thoughtful Estate Plan

Consider a couple in Westerville with a paid-off home worth $500,000, $300,000 in IRAs, and growing brokerage accounts. They want their adult children to inherit smoothly without court delays or public filings. In Ohio, probate for estates with real estate over $35,000 involves public filings, averages 6-12 months, and costs 3-7% of estate value in fees.

This is why many Ohio homeowners ask: should I use a Transfer on Death affidavit or a revocable living trust? The “TOD deed” language you see online often means a Transfer on Death Designation Affidavit recorded with your county recorder’s office.

It’s important to note that Transfer on Death Deeds (TODDs) are not available in all states, which can be a concern for individuals who own property in multiple jurisdictions.

This article compares TOD vs. living trust specifically for Ohio homes—examining probate avoidance, costs, control, creditor risks, and how these decisions fit into broader estate planning. John E. Sestina and Company, a Central Ohio fee-only fiduciary advisory firm, coordinates with estate attorneys to implement these strategies as part of comprehensive financial planning.

What Is a Transfer on Death (TOD) Designation for an Ohio Home?

In Ohio, a Transfer on Death Designation Affidavit (also known as a Transfer on Death Deed or TODD) allows you to name one or more beneficiaries who will automatically inherit your real estate when you pass away. This means the property bypasses probate, the court process typically required to validate a will and distribute property after death. Once the affidavit and death certificate are recorded with the county recorder (e.g., Franklin County Recorder’s Office), property transfers directly to the named beneficiary.

Key characteristics of a TOD for Ohio real estate:

- You keep full ownership and control during your lifetime

- You can sell, refinance, or revoke the TOD without beneficiary consent

- The designation only affects that specific parcel—not bank accounts, investment accounts, or other assets

- Recording fees are typically $34-50 at most Ohio county recorders

A TODD only transfers real estate and does not address other aspects of an estate plan, such as personal property or financial accounts. It also does not provide protection or guidance if the owner becomes incapacitated. Additionally, a TODD does not protect property from creditors or lawsuits after it is inherited by the beneficiary.

For a TOD affidavit to be valid in Ohio, it must be recorded with the county recorder while the owner is still alive. To create a TOD, you must complete the appropriate legal form and file it with the county office; this process is governed by Ohio law.

The core benefit is probate avoidance for that property. However, Ohio TOD rules have evolved since 2009 under ORC 5302.22 and 5302.23, and forms must be properly completed and recorded before death to be valid. County recorders reject roughly 10-15% of submissions for errors.

What Is a Revocable Living Trust for Ohio Homeowners?

A revocable living trust is a legal document where you retitle assets—including your Ohio home—into the trust’s name. Living trusts are recognized in all states, making them widely available for estate planning. You remain in full control as initial trustee while alive and competent.

After transferring ownership, the trust holds title (e.g., “Smith Family Revocable Living Trust dated April 15, 2026”), but you continue living there, claiming homestead exemptions, and can revoke or amend the trust document anytime.

A living trust can provide more comprehensive benefits in avoiding probate compared to a TOD.

The successor trustee role is critical: when you die or become incapacitated, a successor trustee you choose steps in to manage and distribute trust assets without probate court involvement. A living trust allows for the management of assets during the owner’s lifetime and provides instructions for distribution after death. Living trusts can provide for your beneficiaries in the event of your incapacity, allowing a successor trustee to manage your assets without court intervention. To ensure all assets are covered, you must add new assets to the trust as your estate changes. A living trust allows you to retain control over your assets during your lifetime and make changes as your intentions evolve.

Unlike a TOD, a living trust can hold multiple assets simultaneously:

- Your primary residence

- Vacation property in another state

- Non-retirement brokerage accounts

- Business interests

- Bank accounts

- Personal property

A living trust allows you to set specific conditions for how and when your beneficiaries receive their inheritance, providing more control over your estate.

A common failure point: 40-50% of trusts remain unfunded because owners never actually transfer the deed. Your trust must be properly drafted by an Ohio estate planning attorney and then funded with assets to work.

Key Differences Between TOD and Living Trust for Your Ohio Home

Both tools can help you avoid probate for an Ohio home, but they differ significantly in scope, flexibility, incapacity planning, and protection for heirs.

Scope of coverage:

- A tod deed covers one parcel at a time

- A trust functions as a comprehensive estate planning tool covering your entire estate

Timing and control:

- Both allow full control during your lifetime

- Trusts enable ongoing trustee management after death—not just real estate, but personal property and other assets held in trust

Incapacity planning:

- A TOD does nothing if you become incapacitated

- A living trust authorizes a successor trustee to act immediately without court intervention

Complexity and cost:

- TOD: $200-500 total (attorney prep + recording)

- Trust: $1,500-5,000+ upfront, plus retitling effort

- A living trust is more complicated to set up and maintain than a TOD deed, requiring ongoing administration and higher upfront costs.

For Ohio homeowners with one modest home and one capable adult beneficiary, a TOD may suffice. As significant assets and complexity grow, a revocable trust becomes the more practical long-term solution.

A TOD deed is generally better for simple estates, while a living trust is superior for managing complicated family dynamics or potential incapacity.

Flexibility, Control, and Incapacity Planning

Many Ohio families focus only on “who gets the house.” But the bigger issue is often “who can manage the house and finances if I can’t?”

With a TOD:

- You maintain control while alive and competent

- No built-in mechanism exists if you suffer a stroke or develop dementia

- Your loved ones may need durable financial power of attorney or pursue guardianship through probate court—costing $5,000-$10,000 and taking months

- A TOD deed does not provide incapacitated owners an authority to manage property, so a power of attorney is required if you become unable to act.

With a revocable living trust:

- You name a successor trustee in advance (often an adult child or professional trustee)

- If incapacity occurs (defined by your trust terms), that trustee immediately manages bills, home maintenance, and financial decisions without court involvement

Control after the owner’s death:

- A TOD gives the chosen beneficiary full, immediate ownership—they can sell, move in, or mortgage without restrictions

- A trust can stagger distributions, require the home be kept for a surviving spouse, or direct proceeds for grandchildren

Making arrangements such as trusts can help prevent conflict among heirs and spouses, especially in complex family situations involving multiple beneficiaries or potential legal disputes.

Example: A trust can specify “let my spouse live in the house for life, then it passes to my children”—something a beneficiary deed alone cannot accomplish.

Probate, Privacy, and Multi-Property Issues

When someone dies owning assets in their own name in Ohio, the estate generally goes through county probate court—a public process averaging 8.5 months in Franklin County with fees of 4-7%.

How TOD helps: The home passes directly to the named beneficiary and stays out of probate inventory. However, other assets (vehicles, bank accounts, investment accounts without beneficiary designations) may still trigger probate.

How trusts help: A well-funded revocable trust keeps most major assets outside probate entirely—real estate assets, non-retirement investments, and some business interests.

Privacy considerations: Probate filings are public records. While a TOD affidavit is also recorded publicly, the details of who receives all your assets remain more private when transfers occur through a trust rather than a will.

Multiple properties and out-of-state real estate:

- With TOD, you need a separate designation for each property, and out-of-state property follows that state’s law—potentially requiring ancillary probate

- One revocable living trust can hold multiple homes, eliminating multi-state probate issues for Ohio retirees who own property elsewhere

Protection for Beneficiaries: Creditors, Divorce, and Medicaid Considerations

While a revocable trust doesn’t shield your assets from your own creditors during your lifetime, it can offer more asset protection for heirs than a simple TOD transfer.

TOD risks for beneficiaries:

- Once your child receives the house outright, it becomes part of their personal estate

- The home is exposed to their creditors, lawsuit judgments, or divorce proceedings

- If the beneficiary dies or faces financial instability, the property can be lost quickly

How trusts can protect beneficiaries:

- Your trust can keep the home (or sale proceeds) in a separate share managed by a trustee

- Properly designed beneficiary trusts provide better insulation from a child’s health of finances, future creditors, or divorcing spouses

- You can specify distributions only when children reach a certain age

Long-term care and Medicaid:

- A standard revocable living trust does not protect assets from Ohio Medicaid estate recovery

- Neither does a TOD

- Meaningful Medicaid protection requires irrevocable strategies implemented five or more years before needing care

- These decisions require coordination with an elder law firm and financial planner to avoid unintended outcomes

Cost, Complexity, and Common Mistakes Ohio Families Make

Many Ohio homeowners gravitate toward TOD because it seems like an easy fix—minimal paperwork and no attorney needed. But this overlooks potential pitfalls.

Typical TOD costs:

- Attorney preparation: $150-400

- Recording fee: $34-100

- Little ongoing maintenance

Typical living trust costs:

- Upfront legal fees: $1,500-5,000+ for trust document, pour-over will, and powers of attorney

- Deed recording costs to transfer property

- Periodic reviews when circumstances change

Common mistakes with TOD:

- Naming only one beneficiary with no contingency if that person predeceases you

- Ignoring how the TOD interacts with an existing Ohio will

- Using TOD on real estate while ignoring bank accounts and other assets that still trigger probate

- Failing to prepare and update your TOD or trust documents as your circumstances change

Common mistakes with trusts:

- Paying for a trust but never transferring ownership of the Ohio home into it

- Failing to update after refinancing or buying new property

- Not coordinating trust terms with beneficiary designations on retirement accounts and life insurance

- Not adding new assets to your trust as your estate changes, which can leave some assets outside of the trust and subject to probate

Comprehensive Benefits of Estate Planning for Ohio Families

Estate planning is about much more than simply deciding who inherits your Ohio home. For families across the state—including those with blended families or complex relationships—a comprehensive estate plan is the key to ensuring your wishes are honored and your loved ones are protected. By working with an experienced attorney, you can determine the best means to transfer your assets, whether through a TOD, a trust, or another option tailored to your unique needs.

A well-crafted estate plan helps you avoid the delays and public nature of probate, reduce potential taxes, and provide asset protection for your heirs. This is especially important for blended families, where you may want to provide for a spouse while also ensuring children from a previous marriage are not overlooked. The right plan can address these complex situations, offering peace of mind that your intentions will be carried out.

Estate planning is not a one-size-fits-all process. Each family’s situation is unique, and the right approach depends on your assets, family structure, and long-term wishes. By taking the time to create a comprehensive plan—whether that means a trust, a TOD, or a combination—you can help your family avoid unnecessary court involvement and ensure your legacy is preserved according to your wishes.

How TOD or a Living Trust Fits Into Your Broader Financial Plan

Your house is usually just one piece of the picture. High-earning Ohio professionals often have 401(k)s, IRAs, taxable investments, and insurance that must coordinate with any TOD or trust strategy.

It’s important to note that Transfer on Death Deeds are not available in all states, so you should check the availability of this estate planning tool if you own property in multiple states. Living trusts, however, are recognized in all states.

A well-built estate plan aligns with:

- Retirement income planning (when and how heirs inherit pre-tax vs. Roth assets)

- Tax planning (capital gains and step-up in basis on appreciated property)

- Insurance and risk management (life insurance, long-term care planning)

John E. Sestina and Company’s “Managing to Be Wealthy™” process integrates estate planning decisions with cash flow, debt, investment, and tax strategies. Nothing is decided in isolation.

Consider: A dual-income couple in Powell entering retirement might use a living trust for their primary home and investment accounts, while reserving simple TOD designations for certain bank accounts. A business owner in New Albany with rental properties might consolidate everything in one trust to simplify administration for minor children and protect their children’s inheritance.

Including Bank Accounts and Other Assets in Your Ohio Estate Plan

When preparing your Ohio estate plan, it’s important to remember that your home is just one part of your overall financial picture. Assets like bank accounts, stocks, and investments also need to be addressed to ensure a smooth transfer and to avoid confusion or disputes among your heirs. While a TOD deed is a straightforward way to transfer real estate, it doesn’t apply to other types of assets.

For bank accounts and investment accounts, you can often name a beneficiary directly, allowing those assets to transfer outside of probate. However, a revocable living trust offers even greater advantages, as it can hold a wide range of assets—not just real estate—under one comprehensive plan. This approach can help protect your assets from creditors and debts, and provide clear instructions for how and when your chosen beneficiaries receive their inheritance.

The pros of including all your assets in a trust include easier management, greater asset protection, and the ability to set specific terms for distributions. By speaking with an attorney, you can explore the best options for your unique needs and ensure that every asset—from your house to your bank accounts and stocks—is covered. Taking the time to create a thorough estate plan now means your wishes will be respected, your loved ones will be protected, and your family can avoid unnecessary court proceedings and confusion in the future.

Which Is Better for Your Ohio Home: TOD or Living Trust?

For a simple situation—one Ohio home, one adult beneficiary, few other assets—a TOD may be practical. For multi-property owners, blended families, young or vulnerable beneficiaries, or net worth above roughly $250,000, a revocable living trust is usually the better long-term choice.

Choose TOD if:

- Your goal is low-cost, minimal paperwork

- You accept that beneficiaries receive property outright with no protections

- You have a straightforward situation with one property

Choose a revocable living trust if:

- You want incapacity planning built in

- You need to coordinate multiple assets beyond just real estate

- You want to protect beneficiaries from themselves, creditors, or divorces

- Your legacy goals include conditions or staggered distributions

There’s no one-size-fits-all answer. Avoid DIY decisions based solely on forms found online—small technical mistakes can undo what you’re trying to achieve.

How John E. Sestina and Company Helps Ohio Families Decide

John E. Sestina and Company is a fee-only Registered Investment Advisor based in Central Ohio, serving individuals, families, and business owners nationwide with net worth of at least roughly $250,000. Our experienced team has guided clients through estate planning processes for decades, helping them achieve their estate and property transfer goals.

As fiduciaries, the firm does not draft legal documents or sell products on commission. Instead, we:

- Model the financial and tax impact of different estate strategies

- Clarify goals around heirs, charities, and family governance

- Coordinate with independent Ohio estate planning attorneys to implement the right approach

Our collaborative team approach ensures clients receive comprehensive counsel and personalized solutions throughout the estate planning process.

Core services relevant to transferring real estate and property transfers include comprehensive financial planning, investment management integrated with estate considerations, and wealth transfer strategies for children and grandchildren.

If you’re in Columbus or across Ohio, consider scheduling a conversation to review your balance sheet, titling, and beneficiary designations. This article is educational, not legal advice—specific recommendations require personalized review with qualified professionals.

To receive personalized advice or to speak with our team, contact us today. You can fill out our contact form to schedule a consultation and get started on your estate planning journey.

FAQs: TOD vs. Living Trust for Your Ohio Home

Can I use both a transfer on death deed and a living trust for the same Ohio property?

In practice, you normally choose one method per property. If your home is retitled into your revocable living trust, the trust—not you individually—owns it, so a personal TOD affidavit on that property may be ineffective or create legal issues. Many families use a trust for their home and major assets while reserving a new TOD deed or TOD account designations for simpler stand-alone bank accounts. Have an Ohio attorney review any existing TOD affidavits before transferring ownership into a trust to avoid conflicting documents.

Does putting my Ohio home in a revocable living trust affect property taxes or my mortgage?

In most Ohio counties, transferring a primary residence into a revocable trust doesn’t change property tax valuation or homestead exemption eligibility—you’re still treated as beneficial owner. Lenders commonly allow transfers into revocable living trusts without triggering due-on-sale clauses under the Garn-St. Germain Act. Still, notify your lender and confirm the trust language meets requirements, especially before refinancing.

How does a TOD or trust affect the step-up in basis when heirs inherit?

Under current federal tax rules as of 2026, whether beneficiaries receive your Ohio home via TOD or revocable living trust, the property typically receives a step-up in basis to fair market value at the owner’s death. This can significantly reduce capital gains tax if heirs later sell an appreciated home. Tax law changes, so review basis consequences with a qualified professional.

What happens if my TOD beneficiary dies before I do?

If a named beneficiary dies before you and your affidavit doesn’t name contingent beneficiaries, Ohio law may result in that share reverting to your estate—potentially causing probate. Review TOD designations periodically after life events. A revocable trust can contain detailed fallback provisions for multiple contingencies, such as per stirpes distribution if a child predeceases you.

Is a will still necessary if I use a TOD or living trust for my Ohio home?

Yes. Even with TOD or a fully funded living trust, most Ohio residents need a pour-over will to capture stray assets never retitled or given beneficiary designations. A will also lets you name guardians for minor children and address personal property not covered elsewhere. Work with an estate planning attorney to ensure your will, TOD designations, and trust are consistent rather than working at cross-purposes.